T REN DS

Jonathan Labrey, chief strategy officer at the IIRC, talks about the EU non-financial directive and the proliferation of integrated reporting

Integrated vision ELENA K JOHANSSON What impact do you expect the EU nonfinancial directive requiring mandatory reporting will have on corporate behaviour and investments? I can see four impacts. One is that it enables businesses to improve long-term decisions and prepare for the future. Evidence shows that when linking non-financial and financial performance a business can position itself better over the long term because a lot of the non-financial indicators, like human and natural capital, are actually leading indicators of future value. By testing that information against strategy, you are future-proofing it. Managing financial performance, by contrast, is about historical performance. Secondly, from an investment perspective, you will attract more long-term shareholders. Evidence has shown that companies adopting integrated reporting do just this. They provide a much richer set of information, enabling investors to buy into their business models and strategies long term. The third element is changes in capital markets’ dynamics towards more productive and efficient capital allocations. Investors get more confident in projects running upwards of three to five years and can also invest more efficiently. Finally, investors are increasingly saying to us that they are using the quality of corporate reporting as a proxy to understand the quality of business management. Companies producing integrated reporting and non-financial information are proxies for efficient business management. The long-term effect should be that the cost of capital for those businesses reduces: a real benefit for the businesses and for their investors. What are the implications of the move to non-financial reporting globally? Without an environment of transparency and information, investors will increasingly make assumptions, sometimes right and sometimes wrong, which leads to mispricing of market risks, possibly effecting financial stability. A shift to integrated reporting and corporate reporting on the contrary builds up information that aids financial stability, helps price

discovery in the market, and facilitates investments. Investors can understand the true business value. Conversely, businesses that are not fully transparent or don’t price in key risks hinder investors’ capital allocation, leading potentially to market failure. Mark Carney, the governor of the Bank of England and chairman of the Financial Stability Board, has called this the tragedy of horizons. Future risks that lie 10 or 15 years ahead are not priced in today because we are trapped in short-term disclosure horizons of maybe one year or two even though we know that our business models will need to change in five or 10 years because of the impacts of climate change. What is the current state of play of the shift of integrated reporting (IR) into regulation globally? A number of stock exchanges, like Singapore, Johannesburg, Tokyo and Deutsche Börse adopted integrated reporting in a pilot programme, sending a strong signal to the market and encouraging the adoption of IR within those jurisdictions. There is also increasing interest from regulators and political leaders, particularly in Malaysia and Sri Lanka. In South Africa and Brazil there has been regulatory intervention to produce integrated

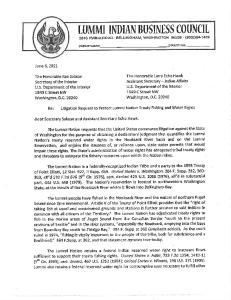

Actual number of integrated reports: top countries 91

27

27

South Netherlands Spain Africa

21

Japan

13

Sweden

Base: N100 companies. Source: KPMG Survey of Corporate Responsibility Reporting 2015

“Investors are increasingly saying that they are using the quality of corporate reporting as a proxy to understand the quality of business management” reporting (on a comply or explain basis). The powerful endorsement of IR by the Japanese government has led to voluntary mainstream adoption by over 200 companies there. What are the challenges for integrated reporting to spread further? One of the biggest is the false perception that integrated reporting is an additional reporting requirement. What we are actually aiming to bring is greater cohesion to the corporate reporting system, to break down silos that have developed over many years and trigger integrated ‘thinking’. We are challenging the culture of corporate reporting. Instead of the past focus on compliance and box ticking, we are saying that reporting starts with the strategy and the business model of the organisation. What’s the future for integrated reporting? It will spread and become a principal of corporate governance rather than a corporate reporting process, because, increasingly, businesses are being asked to account for how they create value now and into the future. Integrated reporting can articulate this to companies with a full range of factors, including its performance on environmental, social, human, intellectual, and financial factors. IR helps businesses with 4 their investors. In an age where we are seeing the growth of ‘stewardship’ codes rather than governance rules, integrated reporting is becoming the information architecture that helps communicate strategy and supports dialogue between a company’s board and its investors. 13