GREATER PITTSBURGH COMMUNITY FOOD BANK Duquesne, Pennsylvania Financial Statements and Supplementary Financial Information For the years ended June 30, 2015 and 2014 and Independent Auditors’ Report Thereon

www.schneiderdowns.com

CONTENTS

PAGE INDEPENDENT AUDITORS’ REPORT

1

FINANCIAL STATEMENTS Statement of Financial Position, June 30, 2015 (with comparative totals, June 30, 2014)

3

Statements for the year ended June 30, 2015 (with comparative totals for the year ended June 30, 2014): Activities and Changes in Net Assets

5

Functional Expenses

6

Statements of Cash Flows for the years ended June 30, 2015 and 2014

8

Notes to Financial Statements

9

SUPPLEMENTARY FINANCIAL INFORMATION Schedule of Expenditures of Federal Awards for the year ended June 30, 2015

17

Notes to the Schedule of Expenditures of Federal Awards for the year ended June 30, 2015

19

Independent Auditors’ Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards

21

Independent Auditors’ Report on Compliance For Each Major Program and on Internal Control Over Compliance Required By OMB Circular A-133

23

Schedule of Findings and Questioned Costs for the year ended June 30, 2015

25

Summary of Prior Audit Findings and Questioned Costs

27

INDEPENDENT AUDITORS’ REPORT

The Board of Directors Greater Pittsburgh Community Food Bank Duquesne, Pennsylvania Report on the Financial Statements We have audited the accompanying financial statements of the Greater Pittsburgh Community Food Bank (Food Bank), which comprise the statement of financial position as of June 30, 2015, and the related statements of activities and changes in net assets and functional expenses for the year then ended and the statements of cash flows for the years ended June 30, 2015 and 2014, and the related notes to the financial statements. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Schneider Downs & Co., Inc. www.schneiderdowns.com

1

One PPG Place Suite 1700 Pittsburgh, PA 15222 TEL 412.261.3644 FAX 412.261.4876

41 S. High Street Huntington Center, Suite 2100 Columbus, OH 43215 TEL 614.621.4060 FAX 614.621.4062

Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Food Bank as of June 30, 2015, and the changes in its net assets for the year then ended and its cash flows for the years ended June 30, 2015 and 2014 in accordance with accounting principles generally accepted in the United States of America. Other Matters We have previously audited the Food Bank’s 2014 financial statements, and we expressed an unmodified audit opinion on those audited financial statements in our report dated November 26, 2014. In our opinion, the summarized comparative information presented herein as of and for the year ended June 30, 2014 is consistent, in all material respects, with the audited financial statements from which it has been derived. Other Information Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying schedule of expenditures of federal awards, as required by Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated November 19, 2015, on our consideration of the Food Bank’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Food Bank’s internal control over financial reporting and compliance.

Schneider Downs & Co., Inc. Pittsburgh, Pennsylvania November 19, 2015

2

GREATER PITTSBURGH COMMUNITY FOOD BANK STATEMENT OF FINANCIAL POSITION JUNE 30, 2015 (with comparative totals, June 30, 2014) Unrestricted General Operating Fund

Temporarily Restricted Grants State Total and Grant Temporarily Programs Fund Restricted

Totals 2015

2014

ASSETS Cash and cash equivalents Cash - Board of Directors designated

$ 2,552,147

$1,297,019

$ 76,610

$1,373,629

$ 3,925,776

$ 3,913,825

136,882 2,689,029 4,495,811 369,977 35,734 1,401,978 62,514 3,527,876 332,699

1,297,019 310,000 543,773 -

76,610 156,902 -

1,373,629 310,000 700,675 -

136,882 4,062,658 4,495,811 679,977 35,734 2,102,653 62,514 3,527,876 332,699

199,154 4,112,979 3,759,046 299,314 2,598,458 88,725 3,828,362 332,699

$12,915,618

$2,150,792

$ 233,512

$2,384,304

$15,299,922

$15,019,583

$

361,836 489,363 7,685

$ 713,053

$ 38,959 35,734 158,819

$

$

$

858,884

713,053

233,512

12,056,734

1,437,739

$12,915,618 -

$2,150,792 -

Investments Receivables Interfund receivables Inventory Prepaid expenses Fixed assets, net Land Total Assets

LIABILITIES AND NET ASSETS LIABILITIES Accounts payable Interfund payables Accrued liabilities Refundable advances Total Liabilities NET ASSETS Total Liabilities And Net Assets

See notes to financial statements. 3

38,959 35,734 871,872

400,795 35,734 489,363 879,557

393,723 548,778 1,133,361

946,565

1,805,449

2,075,862

-

1,437,739

13,494,473

12,943,721

$ 233,512 -

$2,384,304 -

$15,299,922 -

$15,019,583

[This Page Intentionally Left Blank.]

4

GREATER PITTSBURGH COMMUNITY FOOD BANK STATEMENT OF ACTIVITIES AND CHANGES IN NET ASSETS FOR THE YEAR ENDED JUNE 30, 2015 (with comparative totals for the year ended June 30, 2014) Unrestricted General Operating Fund PUBLIC SUPPORT AND REVENUE Public support: Contributions: Donated food $25,117,705 Foundations 1,489,287 Individuals 3,961,266 Corporations 923,457 Community events 650,913 Organizational donations 227,271 Other 217,177 Government grants Total Public Support 32,587,076

Temporarily Restricted Grants State Total and Grant Temporarily Programs Fund Restricted

2014

$25,117,705 2,939,437 3,973,240 1,124,998 674,262 406,313 217,177 6,835,847 41,288,979

$23,514,245 2,955,987 4,104,181 1,204,807 602,449 517,966 214,546 7,365,554 40,479,735

108

2,486,987 321,365 164,011 36,173 84,588

2,371,207 294,596 151,910 21,624 74,489

108

69,950 24,886 10,892 14,925 3,213,777

482,198 34,702 800 15,400 3,446,926

$1,450,150 11,974 201,541 23,349 179,042 5,360,273 7,226,329

$1,475,574 1,475,574

$1,450,150 11,974 201,541 23,349 179,042 6,835,847 8,701,903

2,486,987 321,365 164,011 36,173 84,480

-

-

-

69,950 24,886 10,892 14,925 3,213,669

-

-

Net assets released from program restrictions

8,287,644

(6,811,962)

(1,475,682)

Total Public Support And Revenue

44,088,389

Revenue: Wholesale food sales Shared maintenance Special events Transportation services Investment income Net realized and unrealized gains on investments Miscellaneous income Gain on disposal Membership dues Total Revenue

FUNCTIONAL EXPENSES Program expenses Supporting services Fundraising expenses Total Functional Expenses Changes In Net Assets NET ASSETS Beginning of year End of year

108 108

414,367

-

Totals 2015

(8,287,644) 414,367

-

-

44,502,756

43,926,661

41,324,849 1,392,522 1,234,633

-

-

-

41,324,849 1,392,522 1,234,633

39,224,694 1,491,670 1,026,493

43,952,004

-

-

-

43,952,004

41,742,857

136,385

414,367

-

414,367

550,752

2,183,804

11,920,349

1,023,372

-

1,023,372

12,943,721

10,759,917

$12,056,734

$1,437,739

-

$1,437,739

$13,494,473

$12,943,721

See notes to financial statements. 5

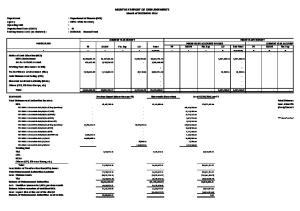

GREATER PITTSBURGH COMMUNITY FOOD BANK STATEMENT OF FUNCTIONAL EXPENSES FOR THE YEAR ENDED JUNE 30, 2015 (with comparative totals for the year ended June 30, 2014)

Food Distribution Donated food distributed Cost of purchased food Salaries and wages Employee benefits Supplies Freight and transportation Printing and advertising Agency support Professional fees Payroll taxes Fees for service Repairs and maintenance Utilities Pension Insurance Postage Garbage disposal Telephone Computer related Travel and meals Conferences Subscriptions Miscellaneous Bad debts Total Functional Expenses Before Depreciation Depreciation Total Functional Expenses

$29,842,079 4,798,363 1,624,055 367,165 87,938 377,037 14,641 24,967 79,795 139,241 21,412 151,556 117,132 91,674 99,744 3,719 32,569 19,183 16,794 12,754 2,663 13,003 1,859 -

Program Services Repack Community and Outreach and Volunteer Education

Network Outreach

$

530,876 76,639 36,782 1,645 46,566 115,031 27,429 44,887 2,038 6,529 4,510 30,727 3,981 3,914 5,481 7,195 14,783 26,368 6,242 352 -

$

289,655 41,768 88,274 890 928 23,991 1,112 12,888 27,721 13,193 16,657 18 21,713 2,251 15,317 1,282 827 1,947 159 -

$

SW PA Partnership

Total Program Services

299,530 38,707 20,394 606 152,514 233 7,311 27,014 1,178 3,795 2,746 19,241 2,291 313 2,276 3,439 7,170 1,866 4,904 101 -

$ 426,425 52,399 45,091 3,984 24,003 9,063 7,780 36,739 1,607 9,375 3,204 22,914 2,969 6,206 4,872 5,973 30,300 4,707 6,041 692 -

$ 29,842,079 4,798,363 3,170,541 576,678 278,479 383,272 238,614 149,294 123,243 271,872 27,347 184,143 155,313 177,749 125,642 14,170 54,282 34,063 48,718 66,289 36,431 32,137 3,163 -

37,939,343

991,975

560,591

595,629

704,344

40,791,882

420,344

20,371

62,074

12,111

18,067

532,967

$38,359,687

$ 1,012,346

607,740

$ 722,411

$ 41,324,849

$

6

622,665

$

Total Supporting Administrative Communications Services

$

698,546 85,097 17,811 4,809 934 71,232 57,483 6,488 5,997 4,627 34,679 3,585 1,587 5,730 7,769 10,445 4,208 17,410 1,023 1,000

Fundraising

2015

2014

Totals

95,099 13,176 1,072 146,050 44,708 7,412 211 989 760 5,083 546 5,584 1,281 1,728 1,167 236 1,091 -

$ 793,645 98,273 18,883 150,859 934 115,940 64,895 6,699 6,986 5,387 39,762 4,131 7,171 7,011 9,497 11,612 4,444 18,501 1,023 1,000

$ 284,030 20,792 77,160 78,104 11,499 163,785 25,903 387,610 3,076 1,998 12,048 1,582 95,812 2,314 40,731 4,643 2,330 7,897 3,157 -

$29,842,079 4,798,363 4,248,216 695,743 374,522 383,272 467,577 161,727 402,968 362,670 421,656 194,205 162,698 229,559 131,355 117,153 54,282 43,388 98,946 82,544 43,205 58,535 7,343 1,000

$28,203,054 4,642,237 3,941,463 577,340 395,457 387,499 371,170 223,841 338,435 342,375 510,758 196,088 160,985 282,793 117,507 109,543 53,734 53,960 90,013 61,927 39,043 52,672 5,620 2,808

1,040,460

326,193

1,366,653

1,224,471

43,383,006

41,160,322

22,261

3,608

25,869

10,162

568,998

582,535

329,801

$1,392,522

$1,234,633

$43,952,004

$41,742,857

$ 1,062,721

$

$

See notes to financial statements. 7

GREATER PITTSBURGH COMMUNITY FOOD BANK STATEMENTS OF CASH FLOWS FOR THE YEARS ENDED JUNE 30, 2015 AND 2014

CASH FLOWS FROM OPERATING ACTIVITIES Changes in net assets Adjustments to reconcile changes in net assets to net cash provided by operating activities: Donated inventory, net change Depreciation Gain on disposal of equipment Net unrealized gain on investments Changes in assets and liabilities: Receivables Purchased inventory Prepaid expenses Accounts payable Accrued liabilities Refundable advances Net Cash Provided By Operating Activities CASH FLOWS FROM INVESTING ACTIVITIES Purchases of fixed assets Purchases of investments Proceeds from sales of investments Proceeds on sale of equipment Net Cash Used In Investing Activities Net (Decrease) Increase In Cash And Cash Equivalents CASH AND CASH EQUIVALENTS Beginning of year End of year

See notes to financial statements. 8

2015

2014

$ 550,752

$2,183,804

521,576 568,998 (10,892) (69,543)

202,857 582,535 (800) (482,095)

(380,663) (25,771) 26,211 7,072 (59,415) (253,804) 874,521

87,049 (131,235) (25,544) 145,607 105,539 (330,612) 2,337,105

(275,598) (668,633) 1,411 17,978 (924,842)

(362,306) (62,183) 2,038 800 (421,651)

(50,321)

1,915,454

4,112,979

2,197,525

$4,062,658

$4,112,979

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014

NOTE 1 - ORGANIZATION The Greater Pittsburgh Community Food Bank (Food Bank) is a nonprofit charitable warehouse that receives food and other products from local, national and governmental sources. The donated, purchased or reclaimed products are then distributed to approximately 380 Southwestern Pennsylvania agencies serving the hungry.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES A summary of significant accounting policies consistently followed by management in the preparation of the accompanying financial statements follows: Use of Estimates - The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Net Assets - The Food Bank classifies resources for accounting and reporting purposes into separate net asset classes based on the absence or existence of donor-imposed restrictions. In the accompanying financial statements, net assets that have similar characteristics have been combined into similar categories. A description of the Food Bank’s net asset categories is as follows: Unrestricted Net Assets - Unrestricted net assets are not subject to donor-imposed restrictions or stipulations as to purpose or use. Unrestricted Board-Designated Assets - Net assets that have been designated by the Board of Directors to provide support for activities that further the Food Bank’s mission. Temporarily Restricted Net Assets - Temporarily restricted net assets are subject to donorimposed restrictions or stipulations that may or will be met either by actions of the Food Bank or the passage of time. The Food Bank reports gifts of cash and other assets as restricted support if they are received with donor-imposed restrictions that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions. Donated Food and Services - The Food Bank receives a substantial amount of donated food from local and regional processors, distributors and retailers. The donated food received and distributed by the Food Bank has been reflected in the accompanying financial statements at the average wholesale per pound value as determined annually by Feeding America, a national network of food banks (See Note 3). The Food Bank pays a value-added processing charge on certain donated food, which approximated $578,000 and $512,000 for the years ended June 30, 2015 and 2014, respectively. These amounts are included within the cost of donated food distributed on the statements of functional expenses. In addition, the Food Bank receives certain donated professional services, which are valued by the donors based on rates commensurate with the type of services performed. These services are reflected in the accompanying financial statements as both revenue and expense. 9

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Revenue Recognition - Revenues from food sales and related fees are reported in the fiscal year in which the food is delivered. Public support consists of grants and donations from governments, corporations, foundations, individuals, other organizations and fundraising activities. The Food Bank generally charges a shared maintenance fee for each pound of donated product shipped to member agencies and affiliated food banks to support the Food Bank’s operational expenses. Cash and Cash Equivalents - The Food Bank maintains its cash balances in local financial institutions, which may exceed federally insured amounts at times. The Food Bank considers all investments with a purchased maturity of three months or less to be cash equivalents. Receivables - Receivables primarily represent amounts due from agencies, partner distribution organizations and government funding sources for services performed and products distributed by the Food Bank. No provision for estimated uncollectible receivables has been made, since management considers all receivables fully collectible. Investments - Investments are carried at fair value with unrealized gains and losses included in the statement of activities and changes in net assets. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Investment income, including interest and dividends, and realized and unrealized gains on investments are reported as increases or decreases in unrestricted net assets unless a donor or law temporarily or permanently restrict their use. Investments received by gift are recorded at fair value on the date of donation. Investment securities, in general, are exposed to various risks such as interest rate, credit and overall market volatility. Due to the level of risk associated with certain investment securities, changes in values of investment securities will occur in the near term, and it is reasonably possible that such changes could materially affect the amounts reported in the statement of financial position. Institutional funds, which are not readily marketable, are carried at net asset value (NAV) as provided by the investment partnerships. NAV is assessed by management to approximate fair value and is used as a practical expedient. In estimating fair value, management takes into consideration valuations reported to the Food Bank by the investment partnerships, the nature of the investments, current market conditions and other factors that the Food Bank considers relevant. The Food Bank reviews and evaluates the values and agrees with the valuation methods and assumptions used in determining the fair value of the institutional funds. Because of inherent uncertainty of valuation in the absence of readily ascertainable market values, the estimated values of those investments might differ from the values that would have been used had a ready market existed for such investments or if the investments were realized, and the differences could be material. Such investments are, by their nature, generally considered to be long-term investments and are not intended to be liquidated on a shortterm basis. Inventory - The inventory of the Food Bank consists of food and other grocery products that are valued at cost except for donated food, which is reflected at average wholesale value as determined by Feeding America. A separate inventory is maintained for goods purchased with state grant program funds. The Food Bank evaluates perishable products on a continuing basis for spoilage, and records the loss of inventory when spoilage occurs, which totaled approximately $1,079,000 and $855,000 during the years ended June 30, 2015 and 2014, respectively, and is reflected as a component of donated food distributed expense on the statements of functional expenses. Based on management’s evaluation of inventory at June 30, 2015 and 2014, no provision for estimated spoilage of inventory has been made.

10

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014 NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Fixed Assets - Fixed assets are recorded at the lower of cost or fair value. Depreciation is provided on the straight-line method over estimated useful lives. Repairs and maintenance that do not extend the lives of the applicable assets are charged to expense as incurred. Gain or loss resulting from the retirement or other disposition of assets is included in total public support and revenue. Management reviews the carrying amount of fixed assets for impairment whenever events or changes in circumstances indicate that the related carrying amounts might not be recoverable. Recoverability of long-lived assets is measured by a comparison of the carrying amount of an asset to future net undiscounted cash flows expected to be generated by the asset. If these comparisons indicate that an asset is not recoverable, the impairment loss recognized is the amount by which the carrying amount of the asset exceeds the related estimated fair value, based on appraisals or other methods to estimate fair value. No impairment loss was recognized in either 2015 or 2014. Refundable Advances - Refundable advances consist of program service fees, government grants and government commodities inventories that are received in advance of the expenditure or distribution to which they relate through program completion or donor stipulation. Income Taxes - The Food Bank is exempt from federal income tax under Section 501(c)(3) of the U.S. Internal Revenue Code (IRC) and is not a private foundation under Section 509 of the IRC. Accordingly, no provision for income taxes is recorded in the financial statements. The Food Bank’s statements of financial position at June 30, 2015 and 2014 do not include any liabilities associated with uncertain tax positions; further, the Food Bank has no unrecognized tax benefits. The Food Bank’s policy is to record interest and penalties related to unrecognized tax benefits as a component of income tax expense, if incurred or assessed. The Food Bank is no longer subject to examination of its tax returns for years before 2012. Subsequent Events - Subsequent events are defined as events or transactions that occur after the balance sheet date but before the financial statements are issued or are available to be issued. Management has considered subsequent events through November 19, 2015, the date on which the financial statements were available to be issued. Recent Accounting Pronouncements - In May 2014, the Financial Accounting Standards Board (FASB) issued accounting standards update (ASU) No. 2014-09, Revenue from Contracts with Customers (Topic 606). This ASU affects any entity that either enters into contracts with customers to transfer goods or services or enters into contracts for the transfer of nonfinancial assets unless those contracts are within the scope of other standards (e.g., insurance contracts or lease contracts). This ASU will supersede the revenue recognition requirements in Topic 605, Revenue Recognition, and most industry-specific guidance. In addition, the existing requirements for the recognition of a gain or loss on the transfer of nonfinancial assets that are not in a contract with a customer (e.g., assets within the scope of Topic 360, Property, Plant, and Equipment, and intangible assets within the scope of Topic 350, Intangibles—Goodwill and Other) are amended to be consistent with the guidance on recognition and measurement (including the constraint on revenue) in this ASU. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The amendments in this ASU are effective for annual reporting periods beginning after December 15, 2018, with early adoption permitted. The Food Bank is currently assessing the impact that the ASU will have on its financial statements.

11

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014 NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) In May 2015, the FASB issued ASU 2015-07-Fair Value Measurement (Topic 820). This ASU removes the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the net asset value (NAV) per share practical expedient. Removing those investments from the fair value hierarchy not only eliminates the diversity in practice resulting from the way in which investments measured at net asset value per share (or its equivalent) with future redemption dates are classified, but also ensures that all investments categorized in the fair value hierarchy are classified using a consistent approach. This ASU is effective for nonpublic entities for fiscal years beginning after December 15, 2016 and interim periods within those fiscal years. A reporting entity should apply the amendments retrospectively to all periods presented. Early application is permitted, which management has elected and has presented the disclosures of investments for which NAV is used as a practical expedient in these financial statements in accordance with this ASU. NOTE 3 - FEEDING AMERICA AFFILIATION The Food Bank is a member of Feeding America, the nation’s leading domestic hunger-relief charity and national network of food banks. In accordance with the financial stability requirement of Feeding America, member food banks are required to maintain a three-month operating reserve in case of emergency situations or demonstrated positive working capital, which is defined by Feeding America as current assets less current liabilities, excluding inventory, in each of the two preceding fiscal years. The Food Bank has demonstrated positive working capital in both the years ended June 30, 2015 and 2014 and, therefore, is not required to establish an operating reserve to meet the Feeding America monitoring requirement. NOTE 4 - RECEIVABLES The Food Bank’s receivables at June 30 consist of the following: 2015 Amounts due from agencies Grants receivable Contributions receivable Miscellaneous

2014

$

172,410 176,870 320,000 10,697

$

139,501 120,640 9,000 30,173

$

679,977

$

299,314

Contributions receivable as of June 30, 2015 consists of $282,500 due in less than one year and $37,500 due in one to five years. NOTE 5 - INVESTMENTS Investments at June 30 consist of the following: 2015 Fair Value Municipal bonds Institutional fund-equity Institutional fund-bond

2014 Fair Value

Cost

Cost

$

5,385 3,113,861 1,376,565

$

5,385 1,928,585 1,259,920

$

5,893 2,276,625 1,476,528

$

5,893 1,189,044 1,331,731

$

4,495,811

$

3,193,890

$

3,759,046

$

2,526,668

12

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014

NOTE 5 - INVESTMENTS (Continued) Investment income for the years ended June 30 is composed of the following: 2015 Interest Dividends

2014

$

219 84,369

$

182 74,307

$

84,588

$

74,489

Investment management fees for the years ended June 30, 2015 and 2014 included in professional fees on the statement of functional expenses were approximately $15,000 and $13,000, respectively. Net realized and unrealized gains on investments for the years ended June 30 are composed of the following: 2015 Net realized gains Net unrealized gains

2014

$

407 69,543

$

103 482,095

$

69,950

$

482,198

NOTE 6 - INVENTORY Inventory at June 30 consists of the following: 2015 Purchased inventory Government commodities - donated Donated inventory

2014

$

879,791 543,773 679,089

$

854,020 903,192 841,246

$

2,102,653

$

2,598,458

NOTE 7 - FIXED ASSETS Fixed assets at June 30 are summarized as follows: 2015 Buildings and improvements Motor vehicles Warehouse equipment Office equipment

$

6,932,201 1,557,272 699,777 596,661 9,785,911 6,258,035

$

6,908,310 1,436,618 684,050 557,598 9,586,576 5,758,214

$

3,527,876

$

3,828,362

Less - Accumulated depreciation

13

2014

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014

NOTE 8 - RELEASE OF RESTRICTED ASSETS Net assets released from donor restrictions by incurring expenses satisfying the restricted purposes or by occurrence of other events specified by donors and grantors for the year ended June 30, 2015 are as follows: Grants and programs: Distribution of government commodities Emergency food and shelter programs Allegheny County Block Grant City of Pittsburgh Block Grant Temporarily restricted donations Other grants and programs

$

State food: Food purchases Administrative funds

4,521,175 203,522 290,648 137,000 1,331,050 328,567

$

1,355,182 120,500

6,811,962

1,475,682 $

8,287,644

NOTE 9 - PENSION PLAN The Food Bank has a defined contribution (money purchase) plan under Section 403(b) of the IRC covering eligible employees. Participants may contribute up to 100% of their pretax eligible compensation, subject to certain limitations under the IRC. In addition, discretionary Plan contributions are made on behalf of eligible, participating employees as a percentage of the participants’ eligible salary. Employer contributions related to the discretionary Plan contribution approximated $137,000 and $199,000 for the years ended June 30, 2015 and 2014, respectively. The Plan also includes a discretionary matching component, and included a match of 3% of eligible wages for both 2015 and 2014. Employer contributions related to the discretionary matching component approximated $93,000 and $84,000 for the years ended June 30, 2015 and 2014, respectively. The Board of Directors has designated cash reserves of approximately $137,000 and $199,000 for the employer contributions to the Greater Pittsburgh Community Food Bank 403(b) Retirement Plan not distributed to employees as of June 30, 2015 and 2014, which was paid subsequent to their respective year-ends.

NOTE 10 - FUNCTIONAL ALLOCATION OF EXPENSES The costs of providing the various programs and other activities have been summarized on a functional basis in the statement of functional expenses. Accordingly, certain costs have been allocated among the programs and supporting services benefited, based primarily on an analysis of personnel time on the related activities.

NOTE 11 - FAIR VALUE MEASUREMENT The Food Bank discloses the category of assets and liabilities measured at fair value into three different levels, depending on the assumptions (i.e., inputs) used in the valuation. Level 1 provides the most reliable measure of fair value, while Level 3 generally requires significant management judgment. Financial assets and liabilities are classified in their entirety based on the lowest level of input significant to the fair value measurement. 14

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014 NOTE 11 - FAIR VALUE MEASUREMENTS (Continued) The fair value hierarchy is defined as follows: Level 1 - Valuations are based on unadjusted quoted prices in an active market for identical assets or liabilities. Level 2 - Valuations are based on quoted prices for similar assets or liabilities in active markets, or quoted prices in markets that are not active for which significant inputs are observable, either directly or indirectly. Level 3 - Valuations are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement. Inputs reflect the administration’s best estimate of what market participants would use in valuing the asset or liability at the measurement date. The Food Bank deems that the carrying amount of cash and cash equivalents, receivables, inventories, accounts payable, accrued liabilities and refundable advances approximate their fair value due to the short-term nature of these assets and liabilities. A description of the valuation methodologies used for assets and liabilities measured at fair value on a recurring basis is as follows: Municipal bonds - The fair value of municipal bonds is determined by market indices and provided by an independent third party. Management has classified its investment in municipal bonds as Level 2 within the fair value hierarchy. See Note 5. Institutional fund-equity - The fund is valued at the net asset value of units, as a practical expedient to estimate fair value. The fund’s assets are invested directly or indirectly in a portfolio of common stocks, and securities convertible into common stocks, of primarily U.S. companies. Additionally, the fund seeks diversity in its portfolio by allocating assets to common stocks and other equity securities of foreign companies and both developed and emerging markets. The fund’s allocation to the U.S. equity market includes exposure to companies in the S&P 500 Composite Index, the benchmark for the fund. Redemptions are effective on the last business day of the month, provided five business days’ advance notice. There were no unfunded commitments as of June 30, 2015. See Note 5. Institutional fund-bond - The fund is valued at the net asset value of units, as a practical expedient to estimate fair value. The majority of the fund’s assets are invested directly or indirectly in dollar-denominated investment grade bonds and other fixed-income securities in an attempt to outperform the broad U.S. bond market. The benchmark for the fund is the Barclays Capital U.S. Aggregate Bond Index. Redemptions are effective on the last business day of the month, provided five business days’ advance notice. There were no unfunded commitments as of June 30, 2015. See Note 5. The preceding methods might produce a fair value calculation that is not indicative of net realizable value or reflective of future fair values. Furthermore, although the Food Bank believes its valuation methods are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of certain financial instruments could result in a different fair value measurement at the reporting date. When available, the Food Bank measures fair value using Level 1 inputs because they generally provide the most reliable evidence of fair value. There were no transfers between fair value hierarchy levels in 2015 or 2014. 15

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO FINANCIAL STATEMENTS JUNE 30, 2015 AND 2014

NOTE 12 - COMMITMENTS AND CONTINGENCIES The Food Bank’s financial and program records are subject to audit by appropriate government authorities in accordance with the terms of the various grant awards and contracts. The government authorities are authorized to review expenditures and to make adjustments. Any normal recurring changes arising from audit after the close of the fiscal year are reflected in subsequent years.

NOTE 13 - MAJOR CONTRIBUTORS Total public support and revenue for the years ended June 30, 2015 and 2014 include food donations made by one corporation that represent approximately 12% and 11% of total public support and revenue, respectively.

16

SUPPLEMENTARY FINANCIAL INFORMATION

GREATER PITTSBURGH COMMUNITY FOOD BANK SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED JUNE 30, 2015

Federal/Pass-Through Grantor Program or Cluster Title Major Programs: Food Distribution Cluster United States Department of Agriculture (USDA): Pass-Through Lawrence County USDA Emergency Food Assistance Program (Food Commodities) Pass-Through Hunger Free Pennsylvania USDA Emergency Food Assistance Program (Food Commodities) Pass-Through Pennsylvania Department of Agriculture USDA Emergency Food Assistance Program (Food Commodities) Pass-Through Allegheny County USDA Emergency Food Assistance Program (Food Commodities)

Pass-Through Lawrence County USDA Emergency Food Assistance Program (Administrative Costs) Pass-Through Hunger Free Pennsylvania USDA Emergency Food Assistance Program (Administrative Costs) Pass-Through Allegheny County USDA Emergency Food Assistance Program (Administrative Costs)

Contract Number

Federal CFDA Number

N/A

10.569

N/A

10.569

1,560,598

N/A

10.569

1,613,742

N/A

10.569

742,959 3,984,101

N/A

10.568

10,062

N/A

10.568

423,144

N/A

10.568

103,868 537,074 4,521,175

165822 168063 165418

14.218 14.218 14.218

22,480 228,168 40,000

50979

14.218

137,000 427,648

Total Food Distribution Cluster United States Department of Housing and Urban Development: Pass-Through Allegheny County Department of Development: Community Development Block Grants/Entitlement Grants Community Development Block Grants/Entitlement Grants Community Development Block Grants/Entitlement Grants Pass-Through City of Pittsburgh Department of City Planning: Community Development Block Grants/Entitlement Grants

Total Major Programs

Amount Expended

$

66,802

4,948,823

17

GREATER PITTSBURGH COMMUNITY FOOD BANK SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED JUNE 30, 2015 (Continued)

Federal/Pass-Through Grantor Program or Cluster Title Other Federal Financial Assistance: United States Department of Agriculture: Pass-Through Pennsylvania Department of Public Welfare State Administration Matching Grants for the Supplemental Nutrition Assistance Program Federal Emergency Management Agency: Emergency Food and Shelter National Board Program - Allegheny County

Total Other Federal Financial Assistance

Contract Number

Federal CFDA Number

4100066909

10.561

FE 32

97.024

Amount Expended

$

59,628

203,522

263,150 $5,211,973

The independent auditors' report should be read with this schedule. 18

GREATER PITTSBURGH COMMUNITY FOOD BANK NOTES TO THE SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS FOR THE YEAR ENDED JUNE 30, 2015

NOTE 1 - BASIS OF PRESENTATION The accompanying schedule of expenditures of federal awards (Schedule) includes the federal grant activity of the Greater Pittsburgh Community Food Bank (Food Bank) under programs of the federal government for the year ended June 30, 2015. The information in this Schedule is presented in accordance with the requirements of the Office of Management and Budget (OMB) Circular A-133, “Audits of States, Local Governments and Non-Profit Organizations.” Because the Schedule presents only a selected portion of the operations of the Food Bank, it is not intended to and does not present the financial position, changes in net assets or cash flows of the Food Bank.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Expenditures reported on the Schedule are reported on the accrual basis of accounting. Such expenditures are recognized following the cost principles contained in OMB Circular A-122, “Cost Principles for Non-Profit Organizations,” wherein certain types expenditures are not allowable or are limited as to reimbursement. Passthrough entity identifying numbers are presented where available.

19

[This Page Intentionally Left Blank.]

20

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

The Board of Directors Greater Pittsburgh Community Food Bank Duquesne, Pennsylvania We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the Greater Pittsburgh Community Food Bank (Food Bank), which comprise the statement of financial position as of June 30, 2015, and the related statements of activities and changes in net assets, functional expenses and cash flows for the year then ended, and the related notes to the financial statements, and have issued our report thereon dated November 19, 2015. Internal Control Over Financial Reporting In planning and performing our audit of the financial statements, we considered the Food Bank’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Food Bank’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Organization’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Schneider Downs & Co., Inc. www.schneiderdowns.com

21

One PPG Place Suite 1700 Pittsburgh, PA 15222 TEL 412.261.3644 FAX 412.261.4876

41 S. High Street Huntington Center, Suite 2100 Columbus, OH 43215 TEL 614.621.4060 FAX 614.621.4062

Compliance and Other Matters As part of obtaining reasonable assurance about whether the Food Bank’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of This Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the organization’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the organization’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Schneider Downs & Co., Inc. Pittsburgh, Pennsylvania November 19, 2015

22

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY OMB CIRCULAR A-133

The Board of Directors Greater Pittsburgh Community Food Bank Duquesne, Pennsylvania Report on Compliance for Each Major Federal Program We have audited the Greater Pittsburgh Community Food Bank’s (Food Bank) compliance with the types of compliance requirements described in the OMB Circular A-133 Compliance Supplement that could have a direct and material effect on each of the Food Bank’s major federal programs for the year ended June 30, 2015. The Food Bank’s major federal programs are identified in the summary of auditors’ results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs. Auditors’ Responsibility Our responsibility is to express an opinion on compliance for each of the Food Bank’s major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the Food Bank’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of the Food Bank’s compliance. Opinion on Each Major Federal Program In our opinion, the Food Bank complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended June 30, 2015.

Schneider Downs & Co., Inc. www.schneiderdowns.com

23

One PPG Place Suite 1700 Pittsburgh, PA 15222 TEL 412.261.3644 FAX 412.261.4876

41 S. High Street Huntington Center, Suite 2100 Columbus, OH 43215 TEL 614.621.4060 FAX 614.621.4062

Report on Internal Control Over Compliance Management of the Food Bank is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered the Food Bank’s internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with OMB Circular A133, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the Food Bank’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of OMB Circular A-133. Accordingly, this report is not suitable for any other purpose.

Schneider Downs & Co., Inc. Pittsburgh, Pennsylvania November 19, 2015

24

GREATER PITTSBURGH COMMUNITY FOOD BANK SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED JUNE 30, 2015

SECTION I - SUMMARY OF AUDITORS’ RESULTS Financial Statements: Type of auditors’ report issued:

Unmodified

Internal control over financial reporting: Material weakness(es) identified?

yes

X

no

Significant deficiency(ies) identified?

yes

X

none reported

yes

X

no

yes

X

no

yes

X

none reported

yes

X

no

Noncompliance material to financial statements noted? Federal Awards: Internal control over major programs: Material weakness(es) identified? Significant deficiency(ies) identified? Type of auditors’ report on compliance for major programs:

Unmodified

Any audit findings disclosed that are required to be reported in accordance with Section 510(a) of OMB Circular A-133? Identification of major programs: CFDA Numbers 10.569/10.568

Name of Federal Programs Emergency Food Assistance Cluster: United States Department of Agriculture (USDA) Emergency Food Assistance Program (Food Commodities)/USDA Emergency Food Assistance Program (Administrative Costs)

14.218

Community Development Block Grants/ Entitlement Grants

Dollar threshold used to determine type A programs:

$300,000

Auditee qualified as low-risk auditee?

X

25

yes

no

GREATER PITTSBURGH COMMUNITY FOOD BANK SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED JUNE 30, 2015 (Continued) PART II - FINANCIAL STATEMENT FINDINGS SECTION This section identifies the significant deficiencies, material weaknesses, fraud and instances of noncompliance related to the financial statements that are required to be reported in accordance with Chapter 5.18 of Government Auditing Standards. None.

PART III - FEDERAL AWARD FINDINGS AND QUESTIONED COSTS SECTION This section identifies the significant deficiencies, material weaknesses and material instances of noncompliance, including questioned costs, related to the audit of major federal programs, as required to be reported by Section 510(a) of OMB Circular A-133. None.

The independent auditors' report should be read with this schedule. 26

GREATER PITTSBURGH COMMUNITY FOOD BANK SCHEDULE OF PRIOR AUDIT FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED JUNE 30, 2014

Finding Number

Finding None.

The independent auditors’ report on compliance should be read with this schedule. 27

Status

[This Page Intentionally Left Blank.]

28